Cracks in the Credit Boom

The recent bankruptcies of Tricolor Holdings and First Brands Group have raised fears of contagion—but are these failures signs of systemic risk or just isolated incidents from bad actors?

With the recent bankruptcies of Tricolor Holdings, a subprime auto lender, and First Brands Group, an auto parts supplier, it seems everyone is worried about what this means for the current environment. Jamie Dimon, whose bank just posted results on pace for another record year of profits, commented in reference to the two implosions:

“My antenna goes up when things like that happen,” Jamie Dimon, JPMorgan Chase & Co.’s chief executive officer, said on a call with analysts. “I probably shouldn’t say this, but when you see one cockroach, there are probably more. Everyone should be forewarned on this one.”

The bankruptcy filings of two-multibillion-dollar companies in the course of a month is not something to ignore. However, if we take a step back to look into what we know so far about these companies’ operations, it seems like it is pretty idiosyncratic.

First, and most importantly, allegations of fraud have been alleged at both companies. First Brands is apparently missing $2.3B that “simply vanished”, according to one of its largest creditors Raistone, a provider of short-term financing that FB relied heavily on. Tricolor, a company who provided auto financing for customers with no social security number or credit history (with interest rates upwards of 20%), has also been alleged of fraud with the DOJ having opened up a probe and creditors looking into whether the company double-pledged the same collateral.

It is completely fair to question whether these companies should have been given so much credit, and that the lenders should have seen red flags, but it seems the fault lies mostly with the companies’ leadership (also noteworthy is that the founder and CEO of First Brands had previously been accused of fraud, which he settled).

These companies were large borrowers in the asset-backed market. First Brands, which reported $11.6bn in total liabilities, was a big user of trade receivable financing, a type of short-term financing that collateralizes the accounts receivables the company is owed from its customers. If the term sounds familiar, it is a similar form of financing that Greensill Capital was providing*, the firm that blew up in spectacular fashion and was a precursor to the collapse of Credit Suisse in 2023. That is not to say these types of financings are inherently risky, but it’s clear it can be abused.

Quick Note: I won’t go deep into the complexities of this type of structured finance product, but what you should understand about trade receivable financing, or factoring, is given the company is collateralizing its receivables, the credit risk you are facing as a lender is not that of First Brands, but of its customers—which were retailers like Walmart and AutoZone and large automakers like Stellantis and General Motors. Again, the alleged fraud here is what seems to be the primary driver of the company’s downfall.

*Greensill Capital’s core product was actually reverse factoring, a much riskier form of trade finance, where they would essentially settle a clients accounts payables by paying off their supplier early and at a discount, then collect the full invoice from the client later down the road

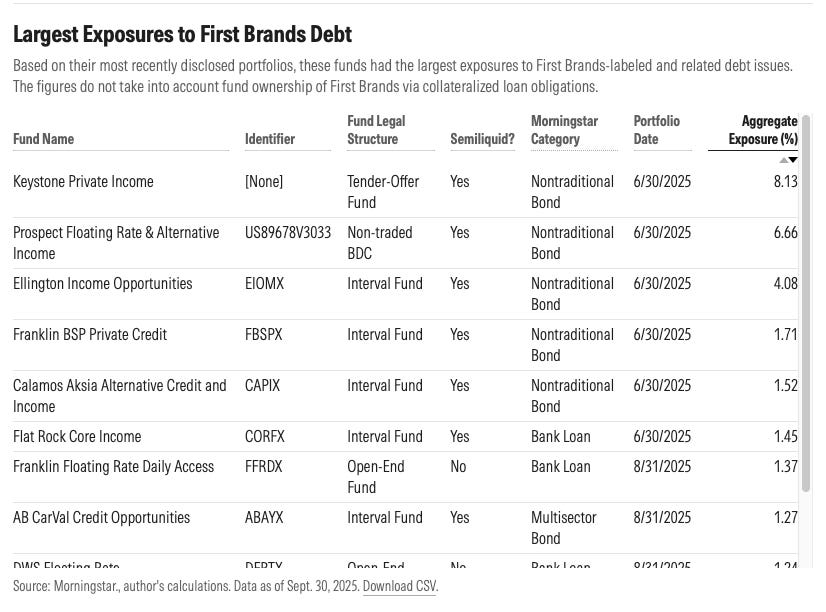

Some have been quick to blame private credit as the culprit, but some of the largest on the creditor list are banks, or attached to banks—Jefferies’s asset management division, Leucadia is reportedly facing ~$750M in losses from FBG. Other major creditors include Norinchukin Bank, ING, and Katsumi Global who together are owed roughly $1B. When it comes to Tricolor: Fifth Third Bank, JPMorganChase, and Barclays are all facing losses in aggregate of over $200M. To be fair, private credit firms were surely involved and are also facing big losses—Raistone is looking for that $2.3B and below is a sort of private credit proxy list with the BDCs/Interval Funds that had the largest exposures to FBG.

Global Demand for Debt

What does this all mean? Are there systemic risks?

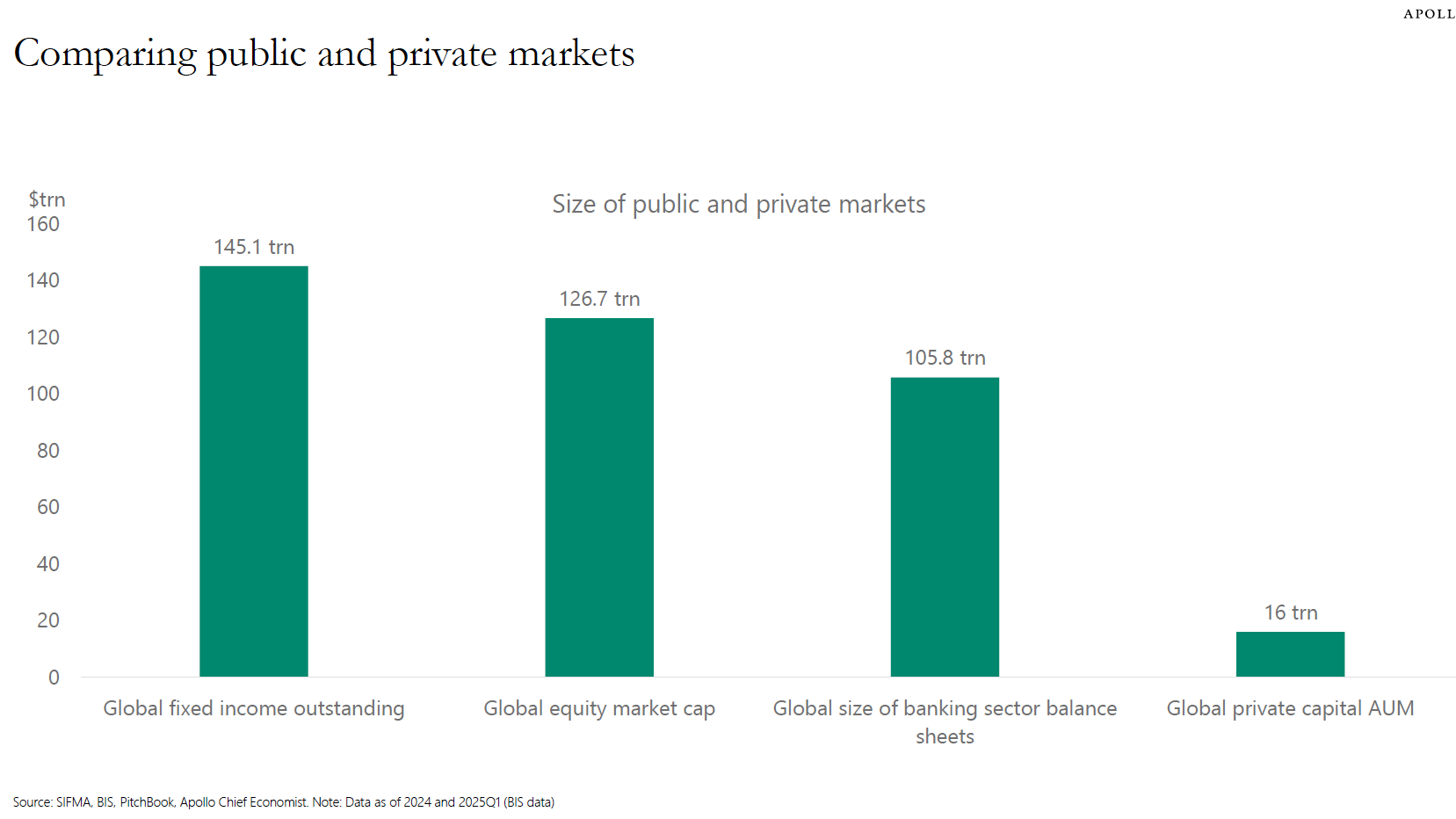

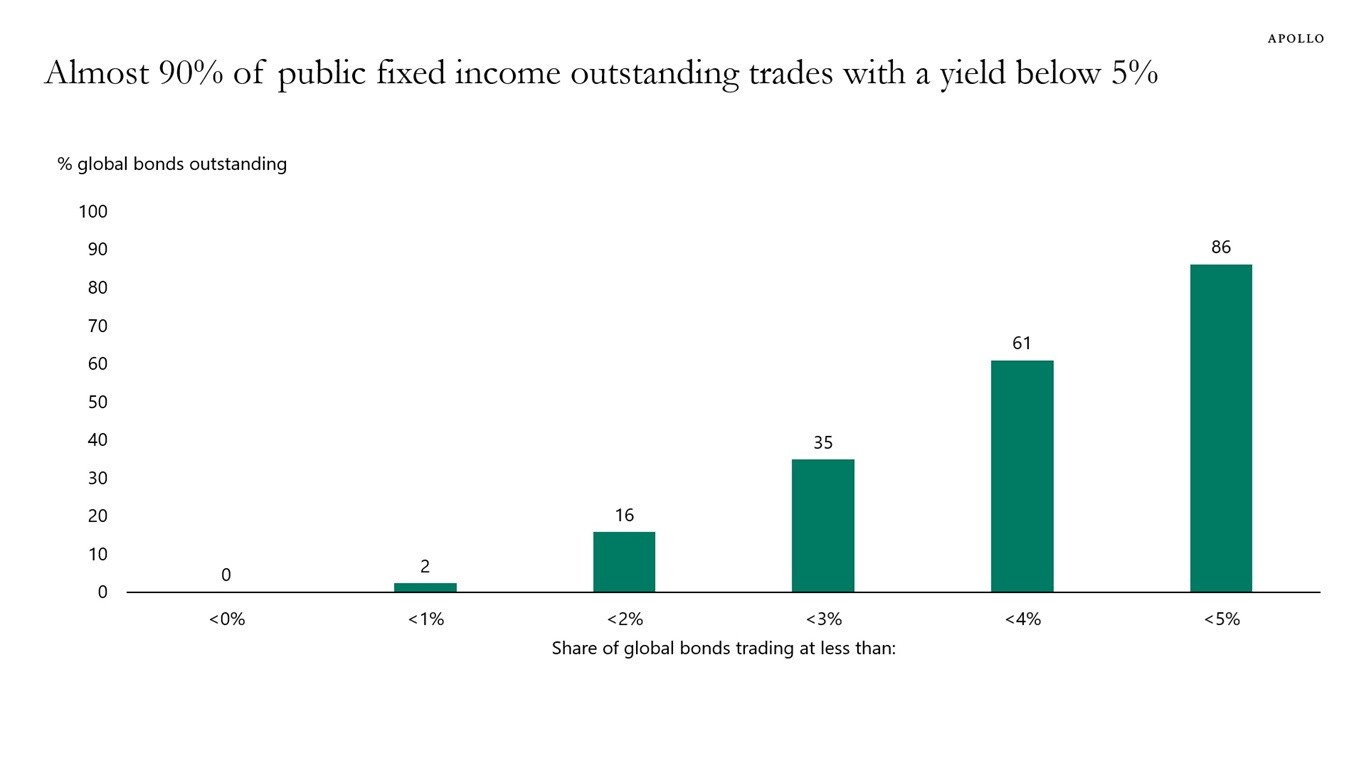

The global demand for debt is strong, with global fixed income outstanding at $145.1T in 2024, and it is clear from spreads tightening, across private credit and public debt, that competition is tough. Banks have shown a willingness to lend in this market just as much as private credit managers. Their balance sheets total $105.8T as of 2024, where private capital AUM is now around 16T.

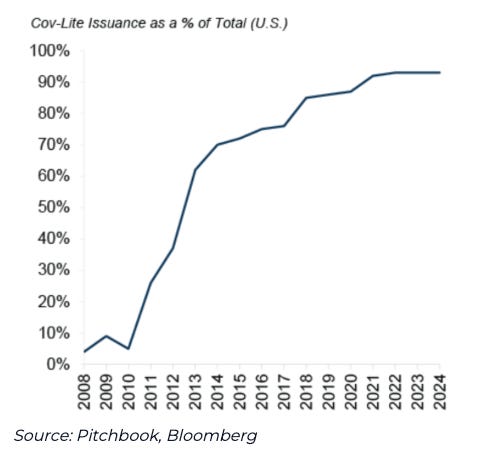

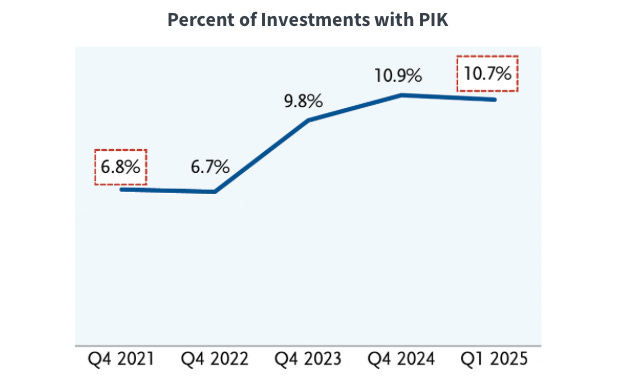

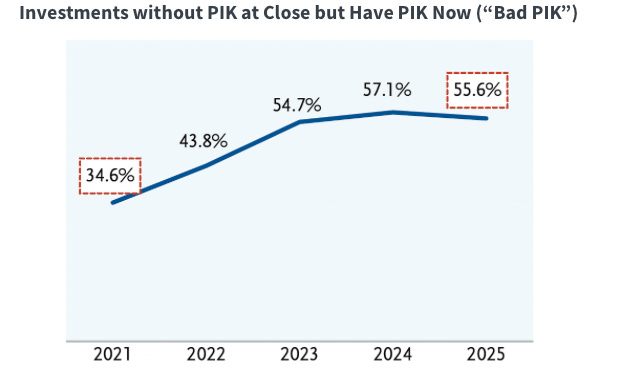

Demand is strong and there seems to be plenty of supply to meet that demand. However, with increased competition some lenders will play loose in order to deploy capital and lighten up their underwriting standards. This can be seen in both the increase of covenant lite loans outstanding and the use of PIK, specifically “Bad PIK”. To define these terms, Cov-lite loans omit the periodic financial tests (such as leverage or interest coverage ratios) that historically gave lenders an early warning system and bargaining power when a borrower’s performance deteriorated. PIK stands for payment-in-kind, a form of interest payment not made in cash but by issuing additional debt (or increasing the principal balance), effectively compounding the amount owed. These types of payments don’t necessarily mean trouble, they can provide borrowers with flexibility and preserve cash. However, Bad PIK, loosely defined as loans that did not have this option at origination, and are instead given as an option to the company during a restructuring of the loan, presumably when they’ve run into trouble.

All of these factors look as if there are risks in the current debt cycle, but is there widespread contagion? Are there risks to the system? I don’t think so. Especially, when considering that the private credit model is just built better than the banking model. In the typical bank business model, you have an institution using very short-term financing or liabilities (i.e., depositor money) to fund long-term assets, such as 30-year mortgages, 10-year corporate/commercial loans, or some complex illiquid trade that their trading desk might do. Private credit, on the other hand, is funding long-term assets, typically middle market commercial loans, with long-term liabilities from investors who are aware of the risks and the illiquidity of their investments, something most bank depositors are not. The industry is better off because it doesn’t have the brutal duration mismatch that the banking model does. If you were to come up with the idea for a bank today, you could surely do better.

I’m not suggesting there are no risks in the debt markets, but when push comes to shove, private credit managers are likely to fare better than banks (helped in part by the absence of mark-to-market valuations).

Disclaimer

The content provided in this newsletter is for informational and educational purposes only and does not constitute financial, investment, or economic advice. The views expressed are solely those of the author and do not necessarily reflect the opinions of any affiliated organizations or employers.

While efforts are made to ensure the accuracy of the information presented, no guarantee is given regarding its completeness, reliability, or suitability for any particular purpose. Readers are encouraged to conduct their own research and consult with a qualified financial advisor before making any investment decisions.

Past performance is not indicative of future results. All investments carry risk, and the value of investments may go down as well as up. The author is not liable for any losses or damages arising from the use of this content.

By subscribing to and reading this newsletter, you acknowledge and agree to this disclaimer.

Sharp analysis of credit market risks - particularly insightful how you've highlighted the trade receivable financing vulnerabilities and the distinction between legitimate factoring versus fraud. The operational credit risks in working capital financing that you outline align closely with trade credit dynamics that TCLM examines. You might find it useful.

(It’s free)- https://tradecredit.substack.com/