Tetra Tech, Inc. (NASDAQ: TTEK)

$8.7B Enterprise Value | $7.9B Market Cap | $30.19 Share Price (04/10/2026)

TTEK, headquartered in Pasadena, California, is a leading provider of high-end consulting and engineering services in water, environment, and sustainable infrastructure. Engineering News-Record has ranked Tetra Tech #1 in Water Treatment and Desalination since 2014.

Investment Summary

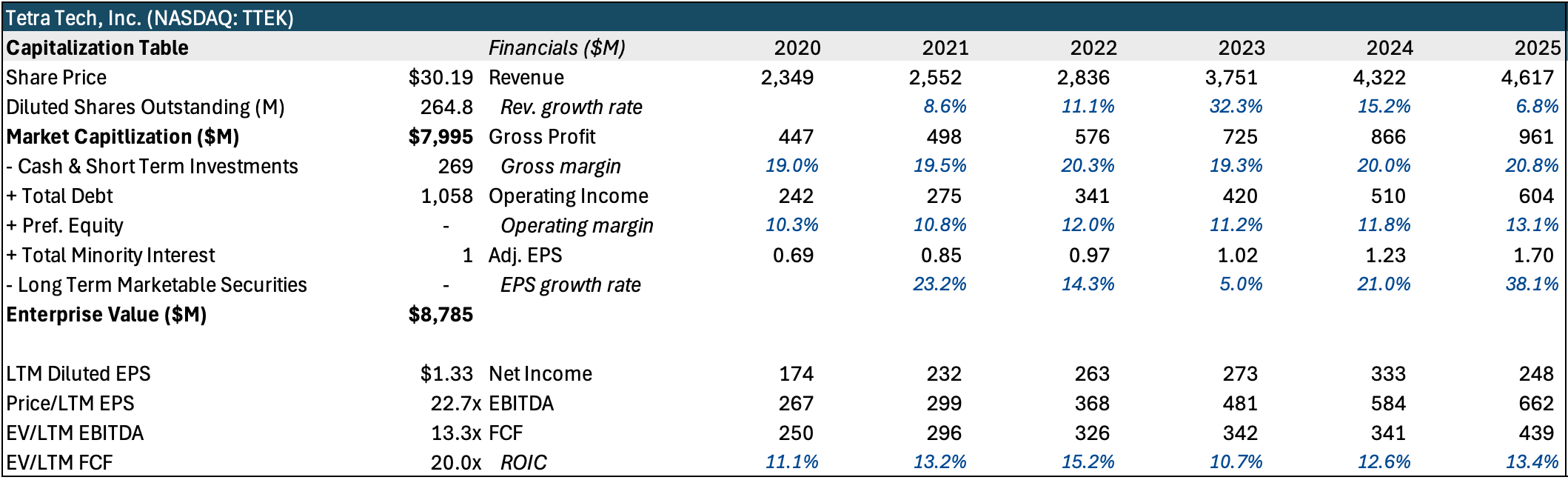

We recommend a long position in Tetra Tech, Inc. at $30.19 per share with a weighted 5-year price target of $85.11, representing a total return of 181.9% (23.0% IRR). The stock trades at 14.1x EBITDA versus a 19.4x five-year average, a de-rating driven by misplaced fears around AI disruption of the consulting sector and the USAID contract cancellations. We believe the market prices TTEK as a cyclical government contractor when it is, in fact, a mission-critical advisory platform with durable competitive advantages and structural margin expansion ahead.

Durable competitive moat in water and environmental engineering. TTEK is the federal government’s institutional knowledge base: its EPA models, datasets, and workflows are structurally embedded across all 10 EPA regions. The company has served the EPA since its founding in 1970 and owns 50 years of proprietary contaminant data on the Great Lakes. When five-year RFPs are issued, there is no credible alternative bidder. State and local water spending and emerging contaminants represent a decade-long structural demand runway the market has not yet priced.

Core compounder with high-ROIC capital allocation. FY2025 ROIC of 13.4% against a cost of capital consistently below 10%. Over the past decade, ROIC has ranged from 11.4% to 16.1%, consistently exceeding WACC. Incremental margins across FY2021 to FY2025 ranged from 11.4% to 29.6%, reflecting the operating leverage embedded in the business as digital tools scale and the revenue mix shifts toward higher-value work.

26 consecutive years of free cash flow generation. Total levered FCF from 2000 through 2025 was $3,882M. FCF grew at a 12.2% 10-year CAGR, driven by rising operating cash flow, a reduction in days sales outstanding from 70 to 57, and lower capex following TTEK’s exit from its construction business. FY2025 FCF was $439M.

13 consecutive years of dividend growth. Quarterly cash dividends have grown at a 12% compound rate. Current dividend yield is 0.86% ($0.26 per share annually). With a payout ratio of only 26% and minimal capex requirements, the dividend has substantial room to continue growing.

Structural secular tailwinds in global water and environmental services. The global water and wastewater treatment market is valued at $348B (2024) and projected to reach $652B by 2034 at a 6.5% CAGR. PFAS regulatory mandates are bipartisan and court validated. International frameworks in the UK and EU mirror the US regulatory trajectory with a 3-to-5-year lag, creating a second wave of demand.

AI is a margin tailwind, not a displacement risk. TTEK trades at a blanket sector discount applied to all consulting firms. Unlike peers, TTEK sits at the far end of the data-defensibility spectrum. Clients fund its R&D while TTEK retains the IP. Proprietary tools like Volans have reduced work that previously required ten engineers over six months to one engineer over three months. The margin benefit accrues to TTEK.

Variant View: What the Market Is Missing